Get the fundraising insights you need

Over the years I've helped over 20 startups raise +$16M in dilutive and non-dilutive capital. Join my monthly newsletter for more insider advice to help you succeed in your next seed-stage funding round.

Once you submit your email, make sure to check your inbox to opt in to the subscription.

Featured

The data room handbook

Learn how to master the data room and use it to achieve fundraising success. This is a comprehensive handbook on fundraising preparation, investors, and the business of startups.

David Steinley

January 20th · 30 min read

Table of contents

Intro

The dirty little secret of successful fundraising is that it actually has nothing to do with tactics, or gentle psychological manipulation, or any other sort of fancy business that gets widely promoted on social:

“10 tips for creating FOMO that’ll close your round 🚀”

That right there is nothing but a distraction. And I’ll tell you why. Because investors are shrewd, and they know what they're looking for. Your best bet is to be utterly prepared with the most investable business opportunity you can conceive of and communicate. Your best case is when you and your prospective investors agree on what the future could be, and they decide they want to bet on this with you.

The reality is that getting to that point of mutual agreement, and excitement, is a nuts and bolts affair. There are no shortcuts. Your success depends exclusively on the quality of your preparation. Whoever is best prepared has the greatest competitive advantage—just like anything else anyone is good at.

It’s pretty crazy working in this space and realizing how unglamorous successful fundraising actually is. At first I thought raising money was like Dragon’s Den or Shark Tank. Pitch, shake some hands, get some cash.

This could not be farther from it. To be sure, there’s a pitch, and the pitch can be exciting, but here’s the shocking part—a pitch, by my assessment, is just the first 10% of what you’ve got to do. Begs the question, what the heck is the other 90%?

What is a data room?

Taking a quick moment to level-set as we begin. I’m going to be using the term data room a lot. Let's agree on what that is.

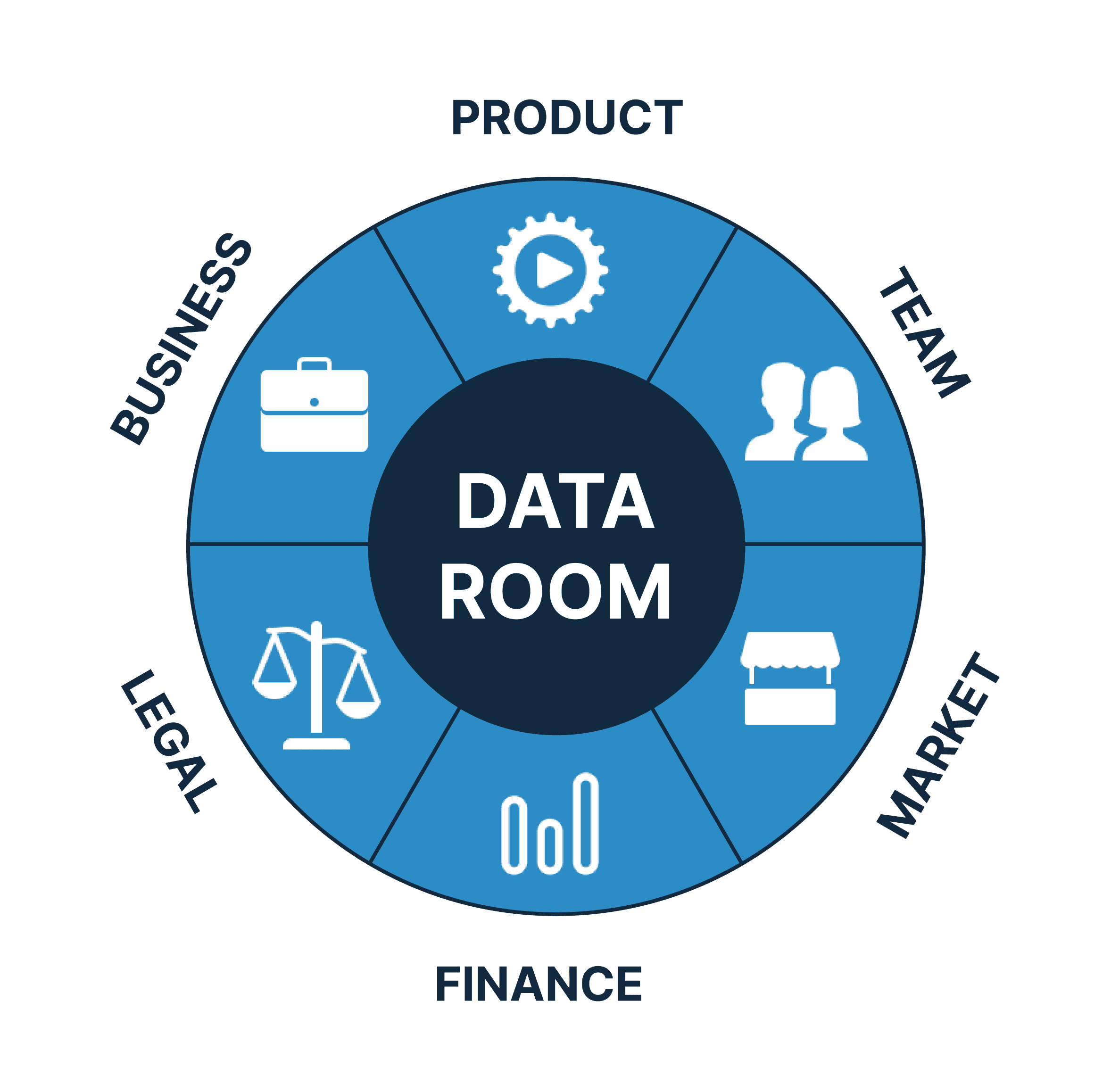

A data room is a repository of files in a shared drive that's generally created around the time a founder decides to sell part or all of their company. For our sake we'll be talking about what the data room looks like for founders raising seed-stage capital. When I'm creating a data room, I organize the necessary files into the 6 sections that you see in the image above.

Seems straight forward enough, so why all the fuss?

Because after working as a fractional CFO for about 6 years now, I've come to realize that having an exceptional data room is one of the most important things you as a founder can do to increase your chances of fundraising success.

A data room will help you find calmness while running a fundraising process which can otherwise be totally overwhelming. It'll show off your professionalism and how seriously you take the success of your business. It'll organize all your most important information in a way that makes your investor's experiences in due diligence with you as frictionless as possible.

This is about what a high-quality, thoughtfully produced data room says about you as a founder, how much authority you've built for yourself, and how it unlocks your ability to get deals done.

Look, when I started working in startups I had no idea what a data room was. And I suspect a lot of people don’t. And that’s all good, because you know what? If you’ve come across this thinking, shoot, I’m just learning now how important this is—don’t beat yourself up. That just means your competition probably doesn't see it this way, and you're about to get an advantage raising capital.

This Data Room Handbook incorporates all of the lessons I’ve learned working for startups as their CFO, helping founders prepare their data rooms so they can raise money successfully. You can find more about my experiences here.

If I do my job right, by the end of this handbook you’ll finally see inside the black box that is fundraising and due diligence, understand how to find calm in the chaotic world of fundraising, and be able to start creating a data room of your own.

I hope you enjoy reading, and let me know what you think.

David

Enjoying this handbook so far?

Just write your email in the box below to sign up to our newsletter. You'll get an email every time we publish a new piece about preparing to raise and increasing your chances of success.

Once you enter your email make sure to check your inbox to opt in to the subscription.

J

Why a data room matters

To get my point across about the value of a data room, it’ll be helpful if I share more about how the fundraising process actually works.

Take Ben Osmond, for example. This is a fictional founder I’ve made up to run a fictional startup I’ve made up called Oyster Tech. I also made up a full data room to back this company up and you’ll see more of its example files as we go through.

The deal is that Oyster Tech is raising a seed round. Ben’s been in discussions with an investor for the past month. Let’s call them Ocean Capital Association. Jill is leading the investment.

Ben and Jill met 6 months before, at an event. Ben said he was thinking of raising later in the year and asked Jill if she wanted to be on his mailing list. (Reader: do this tomorrow if you’re not already. I can’t overstate the importance of having a list and starting with warm connections. This is something that necessarily takes time and cannot be rushed last minute.)

The time came to open the round and Ben got in touch with Jill who had looked at one or two of his newsletters. Just enough to know who he was—enough to get in the game. They went for a coffee and chatted casually for 30 minutes. Jill said she was interested and that Ben should send a deck over. So he did. A meeting was scheduled with a few others from Ocean Capital where Ben was invited to pitch.

Ben left that pitch feeling pretty good and got the email a few hours later saying they’d like to keep talking. I bet you can guess what they wanted to see next.

Ben sent them the link to his data room and the investors were in it, pouring over what Ben only hoped was enough. Now here we are, a month in, nothing more to do now except wait for the good news, right?

For a couple reasons, not really.

The first of which is that this isn’t going to be one pitch and done. There’s going to be follow up meetings with junior members of the investor’s diligence team. There’s going to be meetings with the principles and the partners and the managing partners of the firm. There’s going to be second and third pitches and maybe a fourth.

Meanwhile, Ben’s going to be getting questions. Requests for information. Required to justify why he believes this or believes that. It’s a tiresome affair. And some investors are heavier on diligence and some are lighter. Angels, for example, have a ton of variety in the amount of information they require, and the timelines they do it on. VCs typically require more information. The lead investor always requires more than a follow-on investor who uses the lead’s stamp of approval. And the expectations get higher as the rounds get more advanced.

Now these requests from Ocean Capital alone wouldn’t break the time bank, even if Ben still had to manage Oyster Tech in the mean time. Which he does.

What really makes this process intense is that this isn’t an isolated relationship between one founder and one investor. If Ben want’s to raise $2M, which he does, this is likely going to come from 5 to 10 to even 20 cheques. Some are $25K. Some are $500K. Maybe someone comes in a scoops up the whole round, but it’s doubtful at the early stages because, for an investor, particularly early on, diversification is the name of the game.

This is the point: Many cheques means a ton of concurrent conversations to get the raise done by the self-imposed deadline, a deadline that you should definitely have and shout at anyone who will listen. So now to get the job done we’re talking about a CRM full of 100+ investors, all being pursued at varying degrees, at varying relationship stages, all requiring time and information.

You can see why being prepared matters.

Imagine if you didn’t have the data room and all its files ready (there are 19 files in Oyster Tech’s data room. +/- 5 I’d say this is where you’ll end up too). Imagine if you didn’t know what opportunity you were selling and hadn't a clue how to back it up. Imagine not knowing where your risks were. You’d be blindfolded, utterly overwhelmed with even the most common requests when the request volume is high.

My biggest concern is that when you’re not firm in what you know, it’s all too easy to take every other investor’s opinion to heart, changing up your stuff on the fly, and risk losing what is uniquely yours—your perspective, the value of your experience, your most vigorous information. All because the urge is to say, well, I don’t really know this investment business stuff, so they must be right, and I should make changes.

Whether the changes they suggest are right or wrong (and I would suggest not to make a change unless everyone is saying it), changing out parts mid-flight is version-control chaos and an absolute clusterf**k waiting to happen. Not to mention the loss of your personal power and authority when you give in to the authority of others.

That all sounds like a lot, but you’re in luck because being exceptionally-well prepared means you can avoid all of this headache and focus on what really matters with the folks who one day might just own a consequential part of your business.

When you build a comprehensive data room that tells a truly compelling story about your business opportunity, and when you know how the fundraising process works and you set out your schedule with the right expectations, you can do this.

You can do this darn well, actually.

One final point before we move into how to get a data room for yourself. Investors are who we will focus on during the rest of this handbook, but just think, they are but one member of the ecosystem.

There are grantors who need this info. There are customers who need it. There are partners who need it. Your prospective employees need you to have it. This is your chance to get clear on what your business opportunity really is and to use that understanding to move the ecosystem around you.

What is an investable business opportunity?

Yeah, that's the $$$ question. I'm going to be mentioning this phrase investable business opportunity many times in the rest of the handbook so let me define it up front.

First, let me tell you what it is not. It is not your product. It is not your product because a product alone isn't a business opportunity. It is just that, a product. While in your conversations with customers you might be focused very closely on your product and their needs, that doesn't mean it alone is a sufficient scope to be considered a business opportunity.

I'll tell you why. Because it may be true that you made a product that suits a customer's needs, and they may have purchased it and used it to great effect. But to be an investable business opportunity, an investor needs to see a plausible (or even a theoretically possible) pathway to strong returns. They need a chance of strong returns because your investors also have their own investors. And if your investors can't make money, they ain't gonna be investors for long.

So there's still more questions to be answered to turn your product into an opportunity:

About how many of these potential customers are there? Can you access them geographically? Are they happy with the price? Will your customers get on the phone and vouch for the value of what you're building? How long is the sales cycle with them? How will revenue recur? How can you expand your offering once your first one works?

Who else is offering similar solutions? How big are their businesses? Are they funded? How are you different? What's your unique perspective that makes you comfortable being different? Why is your approach the one that will win in the long run?

Who's on the team helping you build this product? Who's executing the go-to-market strategy? What data do you have on your GTM's effectiveness?

What sort of financing does this need? What do you think you could earn once mature? Can you prove it? How long will it take to get there?

Who's shown faith in what you're doing? Do you have other investors on board? Key hires? Pilots signed? Happy customers? Happy employees? Happy co-founders?

Are you aware of key risks in each of the distinct parts of your business and do you know what you can do about them? Why are you able to tolerate these risks?

And so what is an investable business opportunity after all of this?

It's the full-scope story you're telling about your startup and you're doing it in the form of a data room. Your goal is to communicate a compelling story with forward momentum that looks inevitable while remaining authentic. You got this. Let me show you how.

Enjoying this handbook so far?

Just write your email in the box below to sign up to our newsletter. You'll get an email every time we publish a new piece about preparing to raise and increasing your chances of success.

Once you enter your email make sure to check your inbox to opt in to the subscription.

J

I. Data room content overview

I promised you another 90% of the fundraise came after the pitch. And I wasn’t joking. Below is a screenshot of all the content that I’ve identified over the years as useful for having in your data room.

This doesn’t mean that you need to have all of it or else you’re not going to raise. Quite the opposite—too much info for no reason reduces the chances that your reader gets to the more important points. Take this list only as a completeness check, and build only what you believe is relevant to your business.

How are you supposed to know what’s relevant? If it helps you establish an investable business opportunity, put it in. If it feels like fluff or that you've already said it, leave it out. We'll keep coming back to what makes an opportunity investable further into the handbook.

To give you an idea of size, there's about 19 templated, editable files in the full Oyster Tech data room that I use with my clients, and there could be another 10 or so that are drag and drop documentation for legal purposes only. I didn't mock those legal ones up because they're generally just contracts, not much to play with there.

So take a look at the content list below and let’s review some of the more important sections, the ones you will almost certainly need to create.

And if you want a deeper look, I'll be reviewing these files in the YouTube video that accompanies this handbook, and you can find that at the top of the page. I'd recommend checking it out for some visuals about what all this is about.

Data room index

Here's where you can see all the files in the data room at a glance. It looks a lot like the screenshot just above. The point is for an investor to be able to enter the data room and be immediately directed to this index. From there, they can see what's in it, where they can potentially answer their own questions and not have to ask you questions, and easily jump back and forth between documents they need.

Executive summary

Expect this document to be distributed widely. It's a one or two page summary about the most important elements of your business. After reading, an investor should get the essence of your opportunity. It's a hook. It's like the back cover of a book. It should be exciting enough to want to read more. Don't back up anything you say here, just say it. They'll dig deeper later. This is likely the document you'll want to lead with in your first outreach as well. Either this or a pitch deck, but I prefer this as it's even more simple and easy for investors to distribute among the team.

Another way to do this is to record a video of yourself talking about the content on the executive summary on Loom, etc., and do a little 2 min overview with a bit of demo if you have it. I'd pull up the exec summary on my first tab and then the demo on the second and talk over them, speaking to why this is an investable opportunity.

Investment memo

This is the cornerstone document to the data room. The point is to emphasize in about 15 pages only the most critical information. The benefit to the founder is getting really clear on what matters. The benefit to the investor is seeing at a glance what the most critical information is about the business opportunity. Here's an example from Airbase.

A few procedural points. You can use an investment memo as an index. That means keep the discussion fairly high level. Images are good. Only one or two pages per section. And where you need to go deeper, add a deep-dive file elsewhere in the data room, and link that deep dive back to the investment memo. That way people can go deeper as they choose, but they can also skim the entirety of the opportunity, and hopefully build conviction in it, quickly.

The investment memo would replace the business plan in this case. At the seed-stage you really don't need to do a business plan that's 40 pages in length (except for some govt's). The problem with a business plan is that no investor will read it fully, so you wasted your time prepping it. An investment memo has a much higher chance of being read because it is shorter and more about the compelling information that makes this a business opportunity—it's a sales document, not a how-to manual.

Scale-up plan

Here's where I draw timelines across three main components of the business—product development, operations, and sales targets—all on the same page.

I do this because these things need to work together. You're not going to be selling before you have a product complete, so revenues need to wait. And if you're selling physical products you better have a space up and running with plans to bring down costs, and that too will align with you sales capacity, targets, and cost of sales.

This document looks like a Gantt chart, is made up of activities, milestones, and the timing of it all, and the output also so happens to be the precursor to cash flow modeling.

Product & IP roadmap

This is essentially part of the scale up plans above. Both are timebound and milestone driven. But I would do a separate timeline for product roadmap and IP roadmap that is more detailed. You can overlay your product development milestones along with your IP strategy, discussing in turn each of the key milestones.

Keep in mind when working with timelines that you need to have elements of past, present, and future. What you have done is important to share. That is traction. What you are doing now is how you will spend this round's financing. That's important to be realistic. Then the future you can open up the aperture and showcase why everyone should be excited about the possibilities.

Hiring plan

Here you're showing the experiences and capabilities of your existing team (not job descriptions). You're also showing that there are others who are willing to take a bet on this opportunity, and you. That is social proof.

The 'plans' portion refers to the team you're about to hire with the money you're raising. Generally at the pre-seed and seed stages you're going to be spending about 70% +/- 20% of your money on people, so you've got to be prepared to say exactly why you need them.

You can accomplish a visual with an org chart that exists now and one that you want to exist two years from now, laying out the positions.

Competitive landscape

This is my favorite documents. Writing a detailed competitive landscape analysis is your chance to own what’s likely your most important narrative.

Take a look here at the way a16z explains the biotech tech moment, or how Bessemer talks about markets and creates compelling market maps. They tell a story. There’s anecdotes and personal experiences. There’s a chronology from where we came from to where we are today. There’s data interlaced. It’s not about who’s good and who’s bad. It’s about showing off your constructive, experienced, full-scope understanding of what’s happening out there.

This shows you know how to be differentiated, who you could potentially partner with in the future, and who you could one day exit to. This is the sort of depth that inspires confidence.

Market size analysis

This is all about coming up with the number of potential customers you foresee needing what you're building multiplied by the price you can charge them. This is called a bottom-up market analysis.

Price is never the hard part of the calculation. The hard part is always coming up with the quantity of customers. Because geography matters. Because you need to use approximations. Because it's actually really hard to whittle down customers to the exact right type that is in-market for what you do.

I also like to break customers into small, medium, and large archetypes because that will be more true to the price you can charge each type and that has other downstream effects on your strategy and modeling. I'll be doing a deep dive on this soon.

It's also about backing up the numbers. Make sure you add sources, make sure you show why you believe these folks are actually going to be customers. Add research, references, etc.

Go-to-market strategy

Go-to-market (GTM) strategy defines how you will get your solution into your customers’ hands. The best GTM strategies make use of your unique experiences, perspectives, skills, industry knowledge, connections, and competitive advantages that will allow you to outcompete others with competing offerings.

Being specific is compelling. For instance, you might have an in with a city who can be a pilot customer. You might have an AI stack for cold outreach that is vastly outperforming your peers. You might have a partnership signed that’s going to distribute you all over the internet.

The key lesson is to be specific (and not just copy paste a thoughtless list) and, if you're far enough along, to show off the traction in each of your GTMs so far.

Traction and the sales pipeline

Traction can be shown through a variety of means, which follow a priority sequence about like this: sales and testimonials, paid pilots, sales pipeline and LOIs and waitlists, product development so far, funding so far, key hires, and the list goes on.

Sales pipeline shows the opportunities coming your way. The conversations you're nurturing. I pulled this out specifically because often in the early stages you don't have sales and testimonials yet, and you might be just getting started on your pilots. So I suggest that the best way to back up those significant revenue assumptions is by summarizing all the opportunities in your pipeline, to attempt to quantify them, to show how far out they are from closing, and to use this as evidence that your revenue projections are grounded in reality.

This is more of a B2B approach because admittedly I know that area better. D2C would be more about the waitlists, social following, early-adopters testimonials, etc.

Cash flow model

Here's the financial representation of your business strategies, timebound, and quantified. I believe cash flow models are an excellent way to bring in a totally different look at the exact same business opportunity. Two sides of the same coin, if you will.

The purpose of a cash flow model is to do a few things: to help you with your decision making, to show how you're going to use this round of funds, and to show a plausible pathway to exciting financial results.

As with any model, it's less about the actual numbers are more about the general shape of things and whether there is predictive value. For example, in a climate model, it is not about where the clouds will be, or exactly how many of them there are. It is about the fact that there's a 50% chance of rain, and that you should probably bring an umbrella.

The cash flow model analogy is generally saying, when you sum up all the cash inflows and outflows, is this a business opportunity that, based on the key assumptions you're communicating, could even theoretically make money? And what can you focus on to improve that position?

It's best to do a 5-year cash flow. I have a video about this if you want to check it out.

Cap table and other legal docs

Here's information that is generally drag and drop from the lawyers. Get someone good to do these documents for you because if the documents are not above board at the time you start, you could get stalled for a totally avoidable reason.

Enjoying this handbook so far?

Just write your email in the box below to sign up to our newsletter. You'll get an email every time we publish a new piece about preparing to raise and increasing your chances of success.

Once you enter your email make sure to check your inbox to opt in to the subscription.

J

II. Process to create a data room

The process of creating a data room is the part I love most. It’s where the real value is among all this, and it truly is a creative act.

While the data room itself is a business communications tool, the real question we have to ask ourselves is, what is inside of it? How did that information get there? Is it the right information?

This is the art of it all. This is what separates good from bad data rooms and successful versus doomed fundraising processes.

For the rest of this section I’m going to share about how I actually do this work with founders so that you can get a feel for what it would be like to work together on this, or, if you want to go it on your own, to set you up so you can do that too.

Getting the story straight

We all know things change quickly in startups. And when a fundraising process lasts for 3-6 months, the business might just not respect that you need it to hold on for just a damn minute while you do your raise.

The way around messy reality and ever-changing conditions is to say to yourself, this data room is going to be what it is right now and it is fixed. We're not going to touch it unless we have a really compelling reason to.

Of course, there's balance here. Hold the data room fixed, but don't be obstinate about it. Collect feedback still—as much as you can—and store it in some central document, like a changes-to-be-considered log. Then, if you see feedback all in the same location, make the change. If feedback is scattered and idiosyncratic because so too are the perspectives of the investors looking at this, don't make a change and trust in your preparation and stay grounded in your own beliefs.

The latter is always your go to maneuver. Standing your ground firmly is attractive to a suitor. Being soft and squishy is not.

I want to say more about this firm versus squishy thing. This isn’t one of those psychological maneuvers that I derided at the beginning of this handbook. This is simply a matter of attraction. Every single relationship far as I can tell works like this in practice. This is just being honest to human nature and what we all respect—we respect people who know who they are.

If you are firm in your beliefs, I'll believe you too. If you speak with conviction, I'll say you know your stuff. If you push back from a place of authority, and deep knowledge, I might not agree, but I can respect you and I understand that reasonable people can disagree. Such is the foundation of your authority in the fundraising process.

Where I see the more challenging moments in fundraising is when a founder loses their authority under the weight of the world’s opinions. It’s all too easy because the power balance is so skewed. If you’re building your business, your baby, and you’ve not done it before, and you really need to raise or else you're laying off staff, and you hear all this stuff to the contrary, it’s utterly disorienting. But stay the course. Stay grounded. Remember your preparation. This is why you did the hard work of the data room first.

About story then. I’ve come up with a process for capturing the essence of a startup's story in a simple and coherent way that my client's and I work through together to get us started right. I won’t share too much more about it here unfortunately, and sorry to be cagey, that's not really in the spirit of the handbook, but at the time of writing this I’m actually working on some copyright for this process, so I'll come back to this soon.

What I’ll just say for now is that you've got to look at things like your market, your customer, your problem, your outcomes, your offering, and your domain, and start with this as a sort of lo-fi mock up. Write it all down, make sure it's coherent, keep it simple and small, make it something to use to iterate in quickly, and something to anchor to when the volume of information starts to build.

Mocking up the investment memo

Sort of like I was saying just above—you don’t want to get too deep into things too fast. You need a single place to start, or else your risk going in circles because of all the interdependencies between documents. What you want to do first is create an outline of what really matters.

That means slowing down and taking the time to uncover your most vigorous information: your convictions, perspectives, experiences, observations, anecdotes, testing, and research. Tell me: what have you seen that makes you believe in this opportunity so deeply that you will spend a better part of your working life pursuing it?

That’s what you need to identify, and that’s the real foundation of this whole thing.

Mocking up an investment memo is the best way to get this done. Bring your team. Put everyone in a room. Walk through all the sections in the investment memo and figure out what you really need to say in each of those sections—if you could only add 3 bullets to each section, what would they be?

When I do this with clients this is my favorite part. I’ll ask you all sorts of questions to help bring out the most useful info you have.

A quick heuristic if you want to try this for yourself. Have a meeting with your team and listen for what comes out in casual conversation when you're riffing on your business. Go section by section through the investment memo, thinking about what you really, really need to get across.

Someone is usually like, jeeze, I wish everyone could just see that... xyz. Capture it. This is where the good stuff is. Look for that honest to goodness conviction that everyone has and seems to forget sometimes when the pressure is on. Never get lost in style or business-jargon backwash.

Let’s fill in the data room with supporting documents

Before you build any other file, finish your investment memo. Do the lo-fi mock up above. Then fill it out in a way that you make those key information bullet points central to the story. Maybe each deserves a paragraph of support. Then, whenever you add a file of backup, hyperlink that backup to the relevant part of the investment memo. Once you've finished your investment memo, now you have the cornerstone document of the data room. You have the guide for what else you need to add, which is what this section is about.

At this point, if we were working together, we would sit down and look at the data room index I provided in the previous section. The one with the big list of possibilities. Some will be more important than others depending on the stage of your business and the type of business you are building.

Looking at the index, we would choose what to build next, starting with product, team, and market, which are the core of your business opportunity. Remember, we are telling the story of an opportunity here. Think about each section of the data room with its own individual story, another chance to show where your conviction comes from.

If you're looking for more guidance on how deep to go into any individual section, consider your risk profiles:

If your primary risk is technological, more info is needed in the product folder.

If your primary risk is market-based, more info is needed in the market folder.

How do you know which your risk is? Lots of ways. A really powerful one is to have conversations with friendly investors, mentors, advisors, board members, other entrepreneurs, and to just ask them straight up. You know, test it out. Or another trick is to pay close attention to the questions people ask you. Usually questions are about those things that stick out to them as a concern. I mean, think about your own concerns. You probably know these risks already.

The cool thing about doing this together is that I also get a very intimate knowledge of your business. Deeper than anyone else except for your co-founders typically. That means I can apply the context I have about fundraising raising specifically to your business. This is some of the most important value I can provide you—really helping craft investable plans for the future.

Time and money are next

Now on to the stuff you might have thought this was in the first place: finance, legal, business, summaries, deal terms; money, money, money.

True that this is the way things were. Old school data rooms were about dumping in files for lawyers and accountants to count the beans and parse the terms. (I can say this, I’m an accountant by profession.)

New school data rooms, however, are about showing off an investable business opportunity. There’s beauty in them, story, clarity, founders with depth and authority. So even when it comes to money, we are doing our best to tell a compelling story.

This means we are now talking about the timing of cash flows, the potential size of the reward, and the return on investment you hope you and all your investors will receive.

I know for some founders this business stuff can be anathema. But, stay with me, it’s important. You’ve got to know it. If you don't, you might say nonsense or misguided things that turn off investors. And you risk entering into bad deals. If you want, I have a deep dive on cash flow modeling you can access here on YouTube that walks through all of that in great depth while remaining practical for startups.

Refer to the data room index screenshot and the financial and legal sections at the bottom to get a feel for what sort of content you will need in there. And I’m going to put on my accountant hat and add in one more thing—Get your books and taxes done. Last thing you want is to make it 4 months into a process and then have the counterparty realize that you actually haven’t filed your taxes and you’re looking like a liability now.

High-level documents

Now you can roll up this information even further. Into a pitch deck. Into an executive summary. You can create an Investor FAQ and fill it up with answers to some of the questions you expect to be asked, or have already been asked. Think of that as a self-audit of the files you've created. Or, if we were working together, this could make up part of my final report to you.

It's always easier to create the summaries after you already have the foundational information. This is like creating the underwater section of the iceberg first, and then summarizing the tip of it after the fact. Imagine now, in retrospect, how hard it would be to go the other way.

Fundraising strategies, process, due diligence

This is the part where we say, okay, we have a completed data room. Looks great. I feel great, grounded, secure, confident, authoritative.

Now, what can you do with it?

Well of course you're going to use it to raise money. It's your fundraising foundation, after all. And you could also use it to help you file grants, show to employees in onboarding or use it to pitch them on joining, summarize files for potential customers and partners, and the list goes on to just about everyone in the ecosystem.

If we were working together, this is the final week of our 6 weeks of sessions. My goal is to get you to the point of knowing exactly what you need to know going forward, and how you can proceed:

1) Knowing the amount of fundraising you need, what structure is best, the timing that works, and what your valuation should be. This could be a handbook unto itself so I won't go any deeper here.

2) Understanding the sources of capital available to you, because there's a lot more than just equity investors. I call the entire scope ecosystem financing.

3) Understanding the sort of fundraising process you are running and setting appropriate expectations about the speed and deadlines, who you are reaching out to, how you are nurturing those connections, how you are organizing the information, and the amount of time this will take you.

4) Understanding how diligence works and what to expect during the process.

There's a lot to know, but it's nothing we can't get done right together. And once you know these fundamentals, it's the same thing in the later rounds. To that end, this isn't just an investment now, it's an investment in the continued success of your business and into your ability to close all sorts of deals that come up.

Pitching

Hey, we’re back where we started, and you can see now why I said there's 90% other stuff to do before the pitch.

About pitching itself, we'll certainly review your pitch deck and make sure it's ready for you to head out with it.

I also will want to discuss with you how your ability to tell a crystal-clear story about your business opportunity is what gives you your authority. That means nailing all the business, product, team, market, finance, and legal aspects. Now you can answer questions better, faster, more convincingly, present more clearly, and be someone to take a bet on.

There's lots of storytelling principles that apply here too. I write speculative fiction, and I love talking about the similarities between that and business storytelling. We can go deep here.

Enjoying this handbook so far?

Just write your email in the box below to sign up to our newsletter. You'll get an email every time we publish a new piece about preparing to raise and increasing your chances of success.

Once you enter your email make sure to check your inbox to opt in to the subscription.

J

III. Communications principles

These are some of my observations about what makes a founder successful with their fundraising.

Narrow focus

Current day plans need to be highly focused given startups are always short on money and only have resources to execute well on one thing. The phrase I love is one thing exceptionally well at scale.

And this isn't just narrow as in building one business. It's narrowness across all the individual sections as well. One product, one go-to-market, one customer archetype, one killer feature, one domain of knowledge you're drawing from, one vision for the future. This level of simplicity is exaggerated—you still have to test things out, of course. But just imagine how much more simple and clear your communications would be if you could be this precise.

This, interestingly, is why mature companies tend to be a heck of a lot better at talking about what they do. They know what they do because it actually exists and they have data. That means they can say it with precision.

Early-stage founders don't have data. The future is foggy. So they need to anchor on a set of principles and convictions, and place a bet on some specific outcome for the future. This story is what they are selling, and the more narrow it is, the easier it is to communicate.

Sequences

While the opportunity you're working on right now needs to be narrowly defined, other opportunities are of course available too. But they must happen in sequence. One opportunity, you win it, and then you start another other. As long as this sequentiality is clear in the data room's documents, it's okay to talk about multiple opportunities, just make sure you always emphasize here and now because no one wants to invest in someone who lives too far in the future at the detriment of the next step. (See past, present, and future discussion below.)

These opportunities done in sequence then tend to layer on to each other, i.e. the first wins, then another one is started concurrently and follows the same sort of growth process. Then there are two winners operating and a third begins. Repeat 10 times over and you'll have a full platform with multiple stakeholders. One at a time, in sequence.

Past, present, and future

Everything in startups is happening in a series of time. The key thing is that the information on your timelines be kept separate in time so the information does not collapse in on itself, appearing all at once, and muddying up communications.

Past is useful because it shows the things you’ve achieved. Present is useful because investors (and you) need to know exactly what you’re going to execute on in the short term. Future is about how big this can get, indicating whether this is an exciting opportunity. We can play fast and loose in the future because everyone knows it can’t be known for sure. But for this exact same reason, that’s when you're issued a license to tell a compelling story grounded in only your convictions and principles.

Experience > strategy

Consider all the things you know from experience: the things you’ve tested with clients, the conversations you’ve had with your implementation partners, the things you’ve developed a unique perspective on, the things you know that others don’t, or the things you’ve latched onto that come up in casual conversation all the time that are actually the real truths of the matter.

In the data room, it’s far more convincing to the reader to read through a list of experiences that only you have had. Give them something to really stick to. Information that GPTs generate, in comparison, is slippery. In the early days, there is a significant premium on information that comes uniquely from your own head.

Vigorous information

Think of this as the colorful stuff you bring up in casual conversations, first-hand experiences, testing and results, research, testimonials you’ve received, and the anecdotes you’ve collected. All the stuff that you really know, that really builds your conviction, laid bare. This bottom-up, precise, specific—vigorous—information is what resonates with investors.

Specificity

Specific is compelling in the sense it shows you’ve got the experience to be this exact. It’s colorful in the sense that it creates images in our heads, making it easier to read about and to understand your business. Be specific with text, sure, but also get in there with images and videos and endeavor to create those mental images in the minds of whoever you speak with.

Useful work

The rule in fiction is that each paragraph, each sentence even, should be doing useful work. Same goes for anything in business communications. If you cannot figure out why you’ve included information, remove it. No one ever thanked you for providing too much information.

Said Michelangelo: "I just remove everything that is not David."

Skimmable

Set up headings throughout so that a reader can skim quickly through the documents and get the gist of what’s happening. I write my bold subheaders in the investment memo in a way that someone could read only those phrases and get an idea of what was going on. Then, when they see a subheader they like, they can go deeper into the paragraphs and the supporting documents hyperlinked to the rest of the data room.

Desire

Show off why you care about this when you’re telling your story to people. It's good to be passionate and desirous. Actually, it's mandatory.

Because what this says is that I (playing the role of investor) should care about this too. I see your conviction. I see your care. I see that you are someone who is going to stick with this, and really believes that the future would be better with your solution in it. This makes you someone I really want to buy into and support however I can.

Some investors even say half their investment decision comes down to the founder at the early stages. To that end I guarantee you this investment decision is personal at the early stages, and this is why you need to show up with depth, clarity, authority, and a killer data room.

Enjoying this handbook so far?

Just write your email in the box below to sign up to our newsletter. You'll get an email every time we publish a new piece about preparing to raise and increasing your chances of success.

Once you enter your email make sure to check your inbox to opt in to the subscription.

J

IV. Red flags

These are some of my observations about what messes this up.

Don't require an NDA right away

This is an important point so it gets it's own section. Most investors aren't going to sign an NDA right out the gate. Imagine, they'd be signing hundreds and then they'd have to try to keep track of all of it without getting sued. Impossible, and a huge impediment to speed.

So here's what you do. Make a level 1 (unsecure, public facing) data room and a level 2 (sensitive, deep diligence) data room. Level 1 is good for your first few meetings. And once the process is getting on towards a cheque, you can let them into the NDA-gated data room.

In practice, this might just be holding back on a few files that are particularly sensitive and sending these later. Particularly the details of your GTM and your technology. The principle is the same: public facing first, NDA gated later.

And a list of the rest

Don’t dump in files if you can’t justify why you’re doing it.

Don't have conflicting information because that'll draw questions.

Don’t dilute your message by hedging or saying too much.

Don’t worry about style; substance is more important.

Don’t get back to investors slowly; they’ll appreciate your speed and attention.

Don't go unprepared with a sloppy back-end to your business. Taxes done, books done, legal done. These things will derail the process if you forget about them.

Don’t give away your power in this process; trust in your preparation and never put anyone on a pedestal, no matter how much money they have.

Let's talk if you're looking for some support

As I mentioned at the beginning, I hope that this has been a wide scope overview of the space of raising money. I believe you will now be more prepared for what’s to come, saving yourself the unnecessary overwhelm you might have otherwise encountered, and giving yourself your best chance of fundraising success.

As a CFO—a professional right hand, if you will—I’ve thought for a long time about how I can make this process less stressful for the founders I work with.

Well, this is it. You just read it. As far as I can tell at this point in my career, preparation that unlocks authority and a certain equanimity in an otherwise chaotic process is how I can best support you.

If you want a data room that unlocks your ability to get deals done, reach out to me and we can have a call. I’d love to hear what you’re cooking up.